Building a community of mutual help based on blockchain to solve the pain points of the traditional insurance industry

Blockchain+insurance is an important direction for the financial industry. The mutual assistance guarantee similar to the nature of insurance is a lot of landing scenarios. The essence of insurance is protection, and protection is often to spread risk through mutual assistance. Blockchain smart contracting, centralization and other technologies can improve the operational efficiency and credibility of the field.

The flash chain to be introduced in this paper hopes to use the blockchain to solve the pain points in insurance products. Jin Hui, founder and CEO of Flash Chain, believes that the decentralization, consensus mechanism, openness and transparency, and non-tamperability of the blockchain are highly consistent with the characteristics of insurance. The blockchain + guaranteed track, as well as the HMS reported by MDS and 36æ°ª.

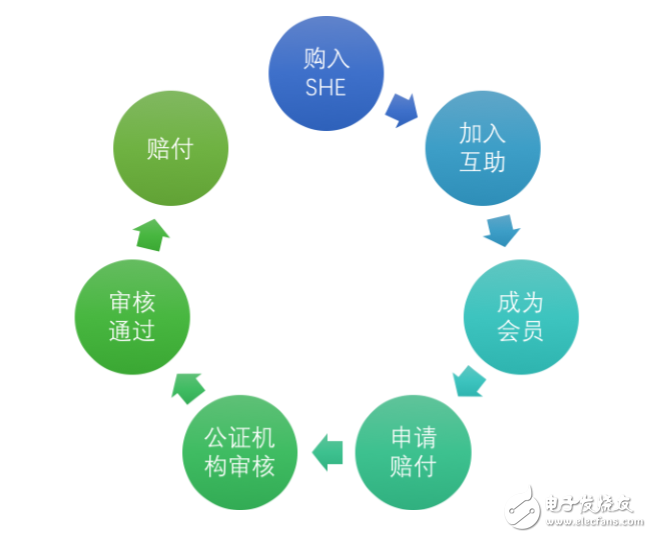

The Flash Chain Program establishes a mutual assistance network. The protection clauses are recorded and executed through smart contracts. After users obtain a certain number of Flash Chain Token SHEs, they can join the specific mutual protection plan by locking the SHE to the asset pool. Member. Once the pre-set conditions occur, the user can apply for a payment, and after review by the notary public, the planned member will share the amount of the payment.

Jin Hui believes that the traditional insurance industry has five major pain points, and can try to use mutual help guarantee + blockchain solutionOne is expensive. Because insurance mainly relies on channel sales, and there are many levels, the premium is expensive. Take Hangyi Insurance as an example, the original insurance products are consumption-type. Once the plane completes a flight, the premium is “splashing water†regardless of whether there is any accident. However, in the flash chain protection plan, as long as there are no members in the plan, the Token in the asset pool will not be reduced, and the members will always be protected.

The second is the issue of trust. In order to increase their brand effect and trustworthiness, insurance companies invest huge amounts of money every year, but still can not prove that the solvency of insurance companies is up to standard. In the blockchain, as long as the locked wallet address is announced, it is known how many people participate in the protection plan and how many Tokens are locked in the pool wallet. These can be transparent and transparent through technology.

The third is privacy protection. This problem is particularly prominent in health insurance products. The information related to health itself is not user-known, but traditional insurance organizations have more or less user data security issues. In the flash chain protection products, in addition to the more special aviation insurance, other products will adopt asymmetric encryption technology. When applying for a claim, you only need to provide your private key to the investigating agency.

The fourth is the issue of insurance fraud. It is understood that the US insurance industry accounts for 10% of the industry's accrued losses for insurance fraud each year. Insufficient compensation (insurance institutions should not be liable, but still paying insurance premiums) is an objective situation in the traditional insurance industry. In the mutual aid program, this issue is more related to the interests of other members. Jin Hui believes that most of the insurance frauds can be detected if the investigation agency investigates objectively and fairly.

The original investigation agency was decided by the insurance company. In the flash chain, the basic qualification conditions of the investigation company were set up by the Flash Chain Foundation, and then the community voted to decide which investigation company to choose. When applying for compensation, the user needs to pledge a certain margin. Once the fraud is found, the deposit is owned by the investigation institution; if the payment is successful, the investigation agency also charges the fee proportionally. This ensures the neutrality of the investigating agency and avoids the payment of accommodation.

The fifth is inflation. For products with a long period of protection, the user gets paid later, and the corresponding purchasing power is lower. This is determined by the inflation problem of the traditional currency, while the Token of the flash chain is issued 5 billion, never issued.

In my opinion, Jin Hui's several pain points are indeed widespread in the insurance industry. Whether it can be solved simply through the blockchain, I have reservations about this, for example, whether the blockchain solves the problem of the ability of offline investigation agencies; Token itself also has price fluctuations, not gold. Is it really resistant to inflation?

However, solving with blockchain is a direction of exploration. At present, the flash chain has been launched on the first product, and the flying wheel has long-term accident protection products. Users lock up 260 SHE join plans, up to 2.6 million SHE or 150,000 USDT. Jin Hui revealed that the product was officially launched on April 11th. At the time of publication, the total number of people exceeded 11,000, and 80% joined through the C2C service platform. For those who do not hold SHE or do not understand digital currency, they can use the C2C service on the Flash Chain Mutual APP to pay the Token to the lock pool participation plan through community volunteers.

Jin Hui said that the idea of ​​the team designing the product is: the probability of occurrence of the event is small, but once it has a great impact on the user, the user market is relatively wide and the accident is easy to confirm. Next, the flash chain is preparing to launch a third-party liability insurance personal supplementary protection plan for auto insurance. This product is mainly for the accident or death of the user when driving, and if the owner's commercial vehicle insurance third party liability insurance is insufficient to cover the compensation amount, the protection plan will be used as a supplementary compensation.

The main profit model of the flash chain is to charge the service fee and the Token that the team implements. The product is currently being deployed in Ethereum, and will build its own public chain in the future, supporting third-party organizations to deploy smart contracts on the flashchain public chain and launch mutual assistance programs. The development plan of the public chain will cooperate with the initial chain, and the future will be forked in the initial chain. In terms of customers, the Flash Chain Mutual Aid is ready to cooperate with the Internet organization to make sales, including various Internet travel platforms, baby fueling, and car clubs around the country.

The Flash Chain team currently has about 50 people. The technical team is based in Beijing and operates in Tokyo. Founder and CEO Jin Hui has 20 years of experience in insurance sales and management; he has served as the founder of China Life Insurance, China People Life Insurance, Sunshine Insurance Executive, Internet Insurance Agent Auto Insurance Platform “Che Xiaobaoâ€; currently Chairman of Sunshine Insurance Agency Co., Ltd. And president. COO Wang Jinlong was the senior business manager of Alibaba Mobile Group. He was responsible for the commercial realization and market cooperation of Ali Games, Ali Literature, UC Browser and other products. After that, he served as the director of easy marketing and the manager of the easy mutual assistance operation. Easily raise insurance, easily manage health and other businesses.

Suizhou simi intelligent technology development co., LTD , https://www.msmvape.com